The insurance industry plays a vital role in the development of economies. Through the years, economies have been able to use insurance products to safeguard investments and generate wealth. The macro impact of insurance products has been facilitated by the principles of insurance, which encourage resource mobilization through the collection of premiums that end up being invested in various financial instruments such as treasury bills and bonds. In turn, these instruments are deployed to develop and maintain vital public amenities hence spurring economic growth. With these and other measures in place, the industry substantially improves efficiency of the entire financial system by injecting adequate liquidity in times of unprecedented crisis.

Historically, developed countries have been able to survive catastrophic events that would have shattered their economies. Notable examples of such events include the Chernobyl disaster of 1986 in Ukraine and Hurricane Katrina in the United States. These events resulted in overall economic losses to the tune of $235 and $161 billion respectively. The overall economic damage from these two events could have dealt a significant blow to these two economies for years to come however, the presence of a stable, vibrant and effective insurance framework enabled these two economies to bounce back to productivity in the shortest time possible.

According to the global status report on road safety by World Health Organization, fatalities resulting from road traffic accidents have increased to 1.3million per year (2018), accounting for a staggering 46% of global traffic deaths. Kenya, being ranked as a lower middle-income country, has experience an increase in road traffic accidents over the last decade. The effects of these accidents have been so severe on vulnerable road users, pedestrians, cyclists, motorbike riders and their passengers. In addition, the announcement of the disputed presidential election results on December 27 2007 led to what could be described as the worst political crisis in Kenya’s post-colonial history. Its effects were uncomprehensive deaths and displacement of people. Recently, an illegally and irregularly constructed man-mad dam located in Solai, Nakuru County, broke its banks, gushing out 190 million liters of water through settlements, leaving in its wake gruesome deaths, horrifying injuries (physical, mental and emotional), massive destruction of property and unprecedented displacement of people. These examples of unprecedented and devastating social, natural and even chemical perils clearly indicate why countries such as Kenya need to enhance, improve and develop the insurance sector.

Developing economies such as Kenya have struggled to sustain economic growth mainly due to inadequate and inefficient measures to withstand economic shocks that stem from the internal and external environment hence leading to restructuring and redistribution of the already limited public coffers. . If appropriate risk mitigation strategies such as purchasing insurance policies by residents were put in place earlier, perhaps these unforeseen shocks could have been absorbed and the effects made less eminent and catastrophic.

The slow development of the insurance industry in developing economies can be attributed to a number of factors such as regulatory pressure, market structure and lack of growth in other financial segments, and social and cultural dynamics. Navigating through social and cultural factors has always been challenging for the insurance industry in Kenya. Different societies have different beliefs regarding risk and this has contributed to slow penetration rates in regions surrounding urban cities such as Nairobi. On a positive note, government’s instruments such as fiscal policy have been deployed to encourage the uptake of insurance products thereby contributing to overall industry growth.

Developing countries may have failed to understand the importance of insurance due to reasons as below:

Low Disposable Income Levels

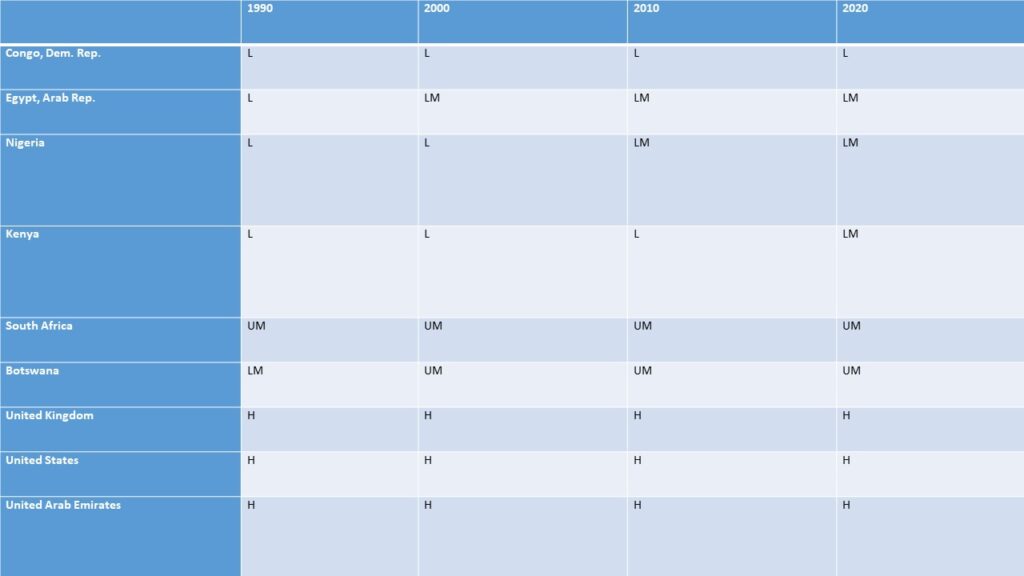

The World Bank often assesses a country’s economic growth and categorizes it as either a low, lower-middle, upper-middle or high-income country. The classifications are updated each year on July 1 and are based on GNI per capita. Kenya was grouped as a lower-middle income country as at July 2020.

L – low income economies, LM – lower-middle income economies, UM – upper-middle income economies, H – high income economies

Income is a central variable in insurance demand model because with higher income, consumers are able to increase their purchasing decisions and this would generate an interest to safeguard their newfound wealth from unexpected risks hence trigger the need to purchase insurance. Whilst this safe income level is yet to be achieved in developing countries like Kenya, the insurance reach is therefore assumed to be far from contented levels.

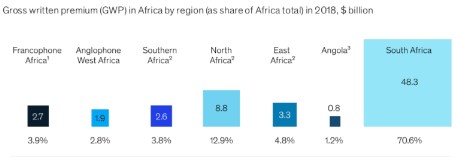

The graph above illustrates an unequal growth in gross written premium in Africa in 2018. Clearly, South Africa dominates the continent registering gross written premium worth $48.3 billion while Francophone countries lagged behind registering gross written premium worth $2.7 billion. A deeper analysis of the graph suggests that regions that have a considerable level of development registered significant levels of growth compared to regions that have been struggling to achieve economic growth due to challenges such as conflict or natural disasters.

Social/Cultural Factors

Religious factors could influence the demand for life insurance in that; there is a low demand for life insurance in many Muslim denominated countries, for instance Egypt and Somalia. This is because the insurance products being provided may not be deemed as Halal or in accordance with the Sharia Law. This factor could also be coupled with low education levels and insufficient general knowledge of the insurance market. Substantial education levels promote the demand for insurance because it increases the level of awareness on the relevant risks and the degree of risk aversion.

Market structure

Developing counties have larger informal sectors compared to formal sectors. This imbalance implies that those in the formal sector are better placed to understand and purchase insurance products. Although the industry has taken steps to reach out to the informal sector, these initiatives have yet to bear fruits and an elaborate communication channel is required if a win-win outcome is to be accomplished.

Marginalization

Marginalization results from unequal distribution of resources. Various regions in Kenya have been socially and economically excluded because of factors such as political alignment and low investor appetite. Marginalized areas are cut off from the national axis of growth due to gross underdevelopment and lack of vital amenities. The availability of basic services such as quality, water, sanitation and security have stagnated growth and led to missed opportunities. When these amenities become available, the society will appreciate the need for insurance as an instrument to mitigate against risks that affect their health, their households and their lives. In addition, these areas will attract potential investors and ultimately seek the need for industrial insurance.

The fact that a sizeable part of Kenya’s population is dependent on agriculture and that macroeconomic instability is higher in developing countries such as Kenya rather than in developed countries, is bound to limit insurance participation in the overall economy. The population uses risk management strategies to alleviate risks, for instance through diversification of crops and other sources of income. However, when it comes to the actual insurance process of acquiring policies, people shun away from this because of the costs it bears.

There is a need for insurance stakeholders such as non-governmental organizations and microfinance institutions, who are involved in insurance schemes, to have close contact with customers. For Instance, KWFT Bancassurance, a subsidiary of Kenya Women Microfinance Bank, provides insurance solutions to clients countrywide. This is because they are widespread in developing countries and therefore they can inspire trust among the clientele. This arrangement has been facilitated by collaborating with leading insurers in Kenya thereby creating a sustainable and interconnected ecosystem within the insurance market. It may also eliminate the insurance premium repayment risks while allowing the MFIs to offer greater benefits to policyholders at better prices. The MFIs could construct channels that enhance premium collection by allowing customers to pay in small installments or through premium financing, thereby reducing policy cancellations. Initiatives such as promoting insurance education could be included in corporate social responsibility programs as a way of creating awareness and marketing insurance products.

In addition to that, the governments should strive to deliver sustainable development projects in marginalized areas around the countries. Kenya, being a low income-economy, road infrastructure development is still lagging as well as health facilities, education standards and basic amenities that a proper economy should have. These amenities should not only be provided, but by also ensuring the policy changes effecting these projects meet international safety standards. This will curb the likelihood of destruction of property and loss of lives arising from poor construction of utilities. It will also lead to the creation of jobs, the betterment of livelihoods and ultimately the increase in investment levels from an individual perspective, which will subsequently have a positive influence over the insurance outreach in the country.

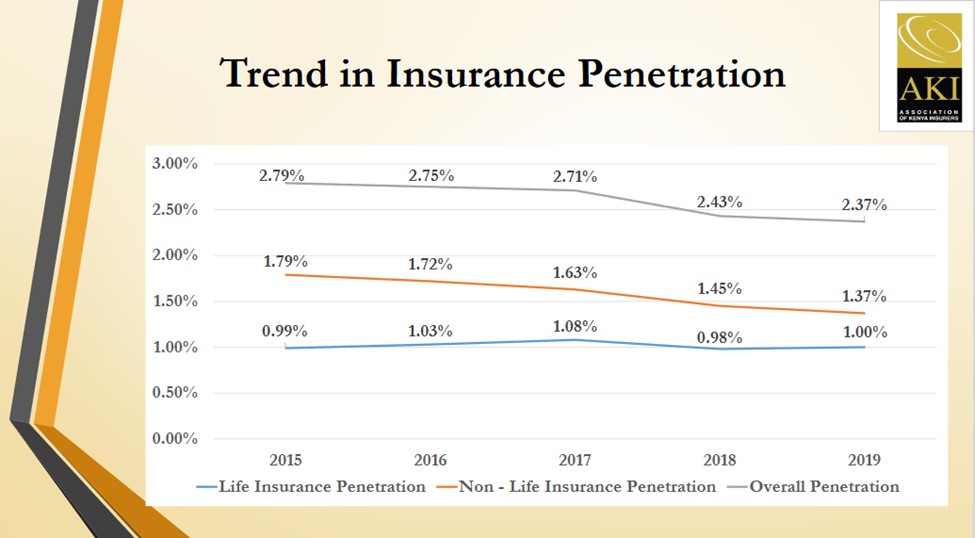

In finality, the Insurance Regulatory Authority, together with the various insurance bodies across the countries, could also review new insurance rates that will be favorable to the economy and the common consumer. According to Association of Kenya Insurers – Insurance Industry Annual Report 2019, there has been a steady decline in the insurance penetration, as illustrated in the figure below. Although Kenya’s insurance penetration rate has been declining over the years, the country’s overall performance vis-à-vis other African countries is impressive. In 2017, Kenya was ranked 6th in the continent ahead of countries such as Seychelles and Rwanda and behind countries such as South Africa and Mauritius.

Association of Kenya Insurers 2019 Annual Report

Miss Kamuu Nyingi is a professional accountant, writer and futurist who possesses a strong desire to understand, simplify and share the interlinkages of various phenomenon and concepts surrounding our lives.