The rise and impact of artificial intelligence globally has been propelled by the growing demand to streamline and ease both individual and corporate systems. This phenomenon has been attributed to globalization and knowledge transfer which began sometime in the 1990s to 2014. Developed countries have been able to capitalize on the benefits of artificial intelligence to strengthen major economic endowments over the years. As the world progressed from the agricultural, industrial, information technology and electrical revolutions, it is clear that artificial intelligence is a key driver of the fourth revolution (digital revolution) currently in play. Artificial intelligence continues to leave its footprint on all industries worldwide. For instance, the financial sector has been quick to embrace AI to facilitate real time exchange of funds though the rate of adoption per region or continentally has varied tremendously.

Evidently, different industries are on the verge of constantly restructuring their processes through modernization and development in machine learning and artificial intelligence. Tesla for instance is accelerating (pun-intended) the world’s transition to sustainable energy with the production of electric cars and renewable energy solutions for businesses. The role of drone technology in the agriculture industry has helped optimize agricultural operations, monitor crop growth and increase crop production. In the insurance industry, Lemonade Insurance, an insurance firm based in New York City, has integrated machine learning in its operations.

The union between insurance practice and artificial intelligence is ideal because the concept of insurance relies on probability and the law of large numbers and artificial intelligence is capable of conducting predictive analytics and simulations. As illustrated in the figure below, insurance operations involve business prospecting, underwriting, premium pricing, renewal notices and after-sale services, claims processing, fraud detection and prevention. Each operation has a defined set of procedures that could easily be automated through machine learning and robotics.

Insurance sales

This is the selling process whereby prospects are approched and insurance deals closed

Underwriting Process

This involves analysing prospective data and reports, with the aim of establishing risk assesment by the insurer

Finance Department

This section involves the accounting of insurance monies received and expenses to be cleared

Claims Process

This is the process of indemnifying the insured after a financial loss

Insurance contract

A seemless transition of these processes ensures effectiveness of the insurance deal

One of the first promising ways artificial intelligence can improve the operations of the insurance industry is through business prospecting (searching and filtering people who need and are likely to purchase insurance products). Currently, the practice involves employing manual techniques such as cold canvassing, referral leads, personal observation, leads from social circles and centers of influence. When analyzing a prospective insurance client, the following metrics are used to assess their level of interest in a product: overall need for insurance cover, ability to pay premium, eligibility and accessibility. Recent developments in the industry have enabled prospective and existing clients to access and assess insurance quotations from different insurers digitally. This has been facilitated by the rise of insurance aggregators who create algorithms that use data from insurance companies to create a digital catalogue of various insurance products. In Kenya, notable insurance aggregators include InsureAfrika and PesaBazaar.com. These advancements have ultimately improved insurance uptake in Kenya hence generating a sustainable growth in gross written premiums for insurance companies.

The second process is the underwriting process. This process begins after relevant proposal forms and reports are filled and presented to the insurer by the prospective client, with the aim of assessing the risks to arrive at a decision of whether to insure a particular risk profile or not. The table below exemplifies such underwriting factors.

Underwriting factors for insurance types

Type of construction of a building, activities carried out in the building, availability of water etc.

Attractiveness of the property, availability of automated security systems, the distance of the property to the police station

Make of the vehicle, use of the vehicle, driving experience of the insured

Having the information above will allow underwriters to price the product accordingly. AI, through machine learning, can enable insurance companies price their policies more competitively and accurately. Information about a person’s city of residence, their driving record and their claim history could be used to accurately figure out how much premium is required and this can easily be generated by using cognitive reasoning . The approximate underwriting time taken could be significantly reduced and the process made much more effective.

Claims processing is another crucial area in insurance operations. Insurance products are considered intangible and its effects can only be felt after a while or after an incident. The management and processes relating to claims are a measure of an insurance performance that can either leave a consumer feeling satisfied with insurance services or disappointed, with the possibility of cancellation or not renewing an insurance cover. The basic claims procedures are depicted in the chart below. It’s important to note that this approach is still being conducted using traditional systems which are manual in nature.

By using cognitive reasoning instruments, the claims process can be a enriched, ultimately leading to less paperwork and improved settlement duration. In addition to this, AI has the ability of detecting fraudulent claims, through the development of algorithms that can identify patterns in data, recognize faults and therefore prevent the possibility of indemnification on invalid claims. The Rise of The Robots article published by Chartered Insurance Institute lets in on Fukoku Mutual Life Insurance, a Japanese insurance company that has replaced human taskforce with Artificial intelligence in its claim processing function and expects to cut its operational costs significantly by £1m a year.

Artificial Intelligence is important in insurance operations because with the dynamic changes in trends, the potential for automation is high. In this midst of COVID-19, the strategic importance of A.I is more paramount than before, due to changes in the nature of risks. Artificial intelligence will have a significant relationship with data analytics. Insurers will be better placed to understand customers’ risks, help businesses reduce risk exposures and find efficient and effective solutions for perils. In addition to this, machine-learning intervention will help companies boost their security details systems and protocols to curb potential digital cyber security threats and attacks. AI seeks to improve the nature of work by; creating new business opportunities while automating tasks. Other areas where Artificial intelligence can take domination in insurance operations include chatbots, document processing and storage and efficient computing (finance operations), by using natural language processing and robotics intervention respectively.

Though the advantages of AI in the insurance industry are immense, its disadvantages are also substantial such as over-technology. Feasibility tests need to be run to determine if AI integration in all insurance operations is necessary. Extracts from the Harvard Business Review on IT and Human Vulnerability compares the future of human lifestyle to a “cyborg” emulation, whereby everything, including affection and love, seems over-technologized and automated. Therefore, it will be paramount to establish AI’s usefulness and suitability in insurance operations. Sure, the insurance cycle will be more efficient with AI, but at what expense, in Kenya – a developing economy, categorized by manual and informal labor that drives the economy?

Secondly, the adoption of artificial intelligence is bound to change the nature of work and skills development among insurance professionals. As the industry strives to attain low-cost efficiency and effectiveness, demand for labor that specializes in information technology and data analytics is set to rise and this might disrupt traditional insurance careers such claim investigators, motor assessors, insurance sales agents and brokers. In addition, as the human-to-human interaction frequency diminishes in the industry, the physical working environment surrounding future insurance employees might evolve to a digitally eco-friendly system.

Third, whilst artificial intelligence will strive to reduce the occurrences of fraudulent claims being reported and indemnified, there will be possible risks in cybercrime and cyberwarfare. Some of these algorithms may be altered intentionally and pose threats on data reserves and ultimately cause havoc on operations and endanger insurance players. Breach of privacy may also be experienced through corporate espionage, since corporations and not individuals will manage surveillance data. Algorithm manipulation may interrupt the ethics and code of conduct of insurance operations. Any algorithm is only as ethically upright as its maker or developer. Should members of a particular taskforce have an ill agenda or motive on a particular insurance player, they may program and influence AI to do exactly that, and its impact will probably exceed measurable lengths.

AI implications will also limit human level thinking since in the end, machines will act only as instructed and programmed.

In finality, insurance contracts are based on principles that guide and govern insurance relations. With AI’s influence on insurance, principles such as utmost good faith may not entirely be relied upon when formalizing these contracts. We will experience disconnect and isolation in human interaction that play a significant role in materialization of insurance business simply because automated decisions and the overall predictive analytics operate on data and produce a decision as an output. Subjecting these insurance principles to a ranking mechanism of developing an output may not be possible.

How feasible is this in Kenya?

According to the survey from the Government AI Readiness Index 2020 by Oxford Insights, Kenya was ranked at position 71 below other African nations such as Mauritius, Egypt and South Africa in its reception, feasibility and adoption of AI within its operations. Kenya’s main challenge in AI adoption is developing a centralized system where data can be stored and harvested, to aid in the development of necessary algorithms. While there is a taskforce dedicated for this already, materialization of strategies remains unwitnessed. It was anticipated that information gathered from the citizenry through the initiative dubbed as Huduma number would be essential for the insurance industry and insurance companies would be granted access to these data silos. However, that remains unspoken of till date.

The use of data in the insurance industry cannot be under-emphasized. In Kenya, insurers are using telematics to enhance the efficacy of motor insurance. One notable insurer, Heritage Insurance, has remodeled its motor insurance product line by offering Autocorrect motor policy. This customized dashboard device helps one to trace and receive feedback regarding their driving style in form of scores. Higher scores are interpreted as satisfactory and safe driving patterns and can be converted to loyalty points that can be redeemed upon renewal with a discount on the insurance premium. Although the uptake has not always been desirable, these examples are evident that AI has triggered development in the industry.

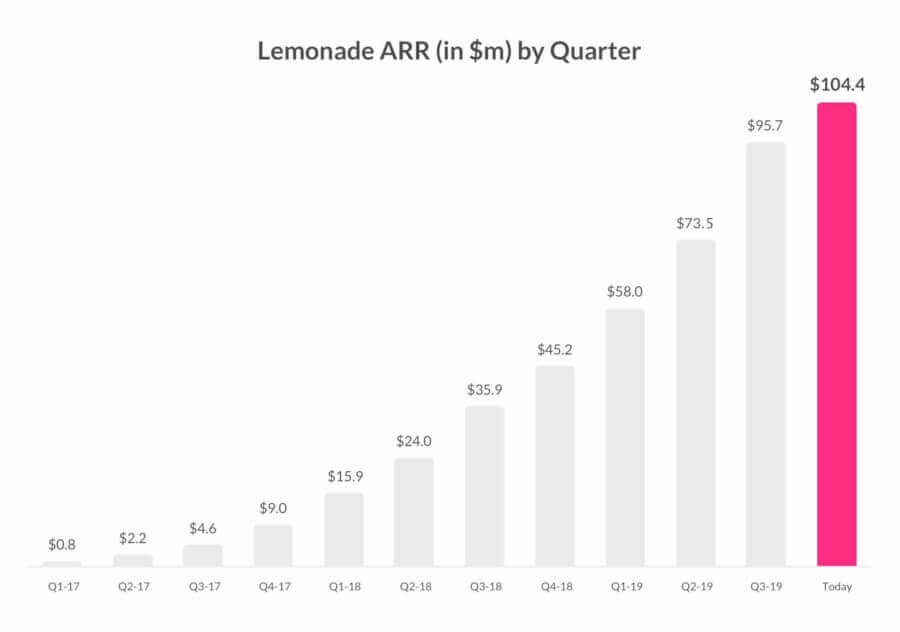

In Kenya insurance premium collected by insurance companies grew from KES 216.1 billion in 2018 to KES 231.3 billion in 2019. The total investments and incomes portfolio has grown significantly by 39% and the total commissions and expenses profile rose from KES 69.6 billion in the previous year to KES 76.3 billion in 2019, as illustrated in the AKI Annual Report 2019. Some of the global insurance trends that have been highlighted include: the adoption of new technologies in claim processing, digital transformation, InsurTech and data automation, expectations of Blockchain technology and Cyber Insurance. If insurance companies in Kenya were to operate a fully automated system, the industry could potentially increase its gross written premiums by 75% by the year 2030. The positive long-term impact of automating systems and using AI, can be best seen when analyzing the quarterly performance of Lemonade Insurance. As illustrated in the graph below, Lemonade Insurance has been able to grow its revenue to $ 104.4 million from $ 0.8 million.

Source: Lemonade.com

More effort by the government, insurance, IT players and other decision-makers need to be vivid and influential. These can be achieved through the following ways:

- The government and the insurance regulatory body needs to develop a workforce of insurance and IT experts, who will oversee not only the feasibility but also the value addition of AI in the industry. Efforts should not be in over-technologizing but in value-addition.

- Ensure codes of conduct are also put in place, to ensure that the principles of insurance are still adhered to. This is because there could be a possibility or a risk probability of marginalization. For example, gender biasness in insurance pricing. The algorithms could portray data biasness, which subsequently may deflate the insurance operations. System transparency and credibility measures need to be observed constantly.

- The government needs to develop the skill and agility required in the digital spaces. For instance, through investments in machine learning, mentorship programs in schools and creating engagement platforms where digital opportunities are discussed. As it stands, most insurance players do not know much about the theory and practical implications of AI in insurance. Therefore, investment in the education sector and training facilities in IT by the government will support the evolution of insurance operations.

As it is evident that the advantages of Artificial Intelligence is immense, it will be paramount for the insurance industry players to distribute evenly the functionality of AI and to equate its precedence with the need of actual human involvement and intervention, so that the benefits and the values cut across evenly. Local insurance companies require more time to learn from other industries and countries on how to integrate operations with AI. As the industry contemplates migrating to a digital system, there is need to ensure a seamless and less disruptive transfer from traditional platforms. Artificial intelligence done right will empower however, it should not necessarily equate to a loss of human intervention in exchange for the convenience of keeping up with technological standards. Artificial intelligence should strike a balance between the two, such that a more complimentary model is developed and enforced.

Miss Kamuu Nyingi is a professional accountant, writer and futurist who possesses a strong desire to understand, simplify and share the interlinkages of various phenomenon and concepts surrounding our lives.